Schrodinger $SDGR

Notes and highlights from different write-ups on the biotech company Schrodinger

Dom’s Deep Dive on Schrödinger (Feb 2021)

Schrödinger’s mission statement says it all, “To improve human health and quality of life by transforming the way therapeutics and materials are discovered.

Two new oncology drugs already being FDA approved and several phases I and phase II trials beginning for other drugs.

This has been the case for Schrödinger as President and CEO Ramy Farid, Ph.D. has been committed to working for Schrödinger for the last 19 years. The company’s co-founders Richard Friesner and Bill Goddard are still involved and on the board of directors to provide additional guidance.

Schrödinger has a 4.6 out of 5-star rating on Glassdoor for being a great place to work at. Ramy has a 96% rating on Glassdoor as CEO and the company has a 91% recommendation to a friend rating for being a great place to work at. Schrödinger made the 2019 and 2020 Crain’s Best Place to Work at in NYC List and made the Top 10 out of Best 100 Companies to work at on BuiltinNYC.com.

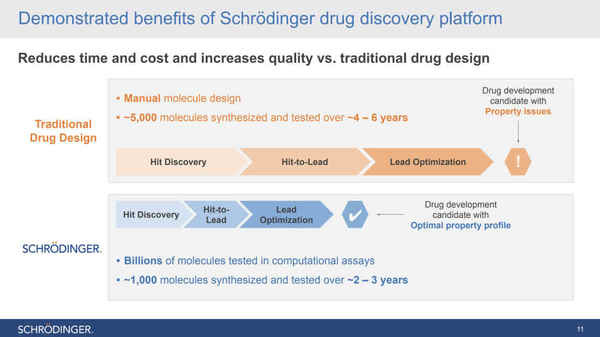

Their physics-based computational platform enables collaborators to discover high-quality molecules faster, at lower costs, and with better accuracy than traditional trial by error methods of drug discovery. What may take a company five or six years to get a drug discovered & ready for clinical trials sometimes may take only two or three years & have an optimal property profile for the trial.

Schrödinger already has over 10 different company collaborations going on right now globally and some are in IND enabling phases, phase 1, or even phase 2 clinical trials. Schrödinger also has gained equity positions in their collaborators and other co-founded companies such as Relay Therapeutics.

The molecule simulation platform that Schrödinger has can be utilized for new materials in other industries such as energy with batteries, fuel cells, and hydrogen storage materials, organic electronics, and polymers, and soft matter. The Schrödinger platform is the foundation of design for novel materials in several industries such as aerospace, energy, semiconductors, and electronics.

Schrodinger: High Margins, Sticky Business, Incredible Upside (May 2021)

https://seekingalpha.com/article/4431776-schrodinger-high-margins-sticky-business-incredible-upside

[You will probably learn more about the company’s platform and the industry by reading through the comments section of the write ups on Seeking Alpha. Especially by users like ‘WarrenJF’ & ‘YCS186’.]

Drug Discovery has historically been the most expensive and lengthy step in creating new drugs. SDGR’s physics-based software cuts the time in half as well as the costs.

Along with being a software company with 80% GMs, 99% customer retention rate and robust growth, they have their preclinical drug pipeline giving them major upside.

Bill Gates and billionaire healthcare tech hedge fund titan David E. Shaw are early investors and currently own ~27% of the outstanding shares.

SDGR’s proprietary physics-based software is fundamentally changing the drug and material discovery process. Rather than designing molecules by hand, SDGR’s software tests billions of molecules in computational assays. This step filters it down to the best possible ~1,000 molecules. Then through further simulations in the software, users are able to identify the best molecules to advance with. The entire discovery process takes only 2-3 years. Users also identify molecules that have a higher likelihood of success at commercialization because computer-generated molecules are inherently more stable than molecules made by hand. Their software makes this costly and lengthy initial step cheaper, quicker, and more efficient.

The platform is able to evaluate billions of molecules per week compared to traditional methods evaluating ~1000 molecules per year. Traditional methods test significantly fewer molecules because it is nearly impossible to predict properties of molecules without going through the entire process of chemical synthesis, taking weeks to conduct in a lab. In contrast, SDGR’s software simulations are capable of accurately predicting critical properties of molecules, which allow researchers to selectively synthesize molecules with more optimal properties, leading to more stable molecules that will have a higher likelihood of success at commercialization.

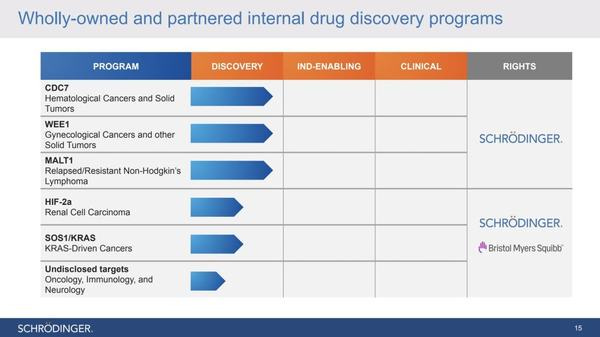

Their goal is to submit up to three IND applications in 2022, with the first coming in the first half of 2022. She was very positive about their wholly-owned programs CDC7, MALT1, and WEE1, which are all enzymes involved in the replication of cancer cells. The thesis is that they will slow or completely cut off the replication process of cancer cells.

SDGR was founded in 1990 with the goal of using the power of computing to better conduct scientific research.

To focus on developing cutting-edge molecular software programming, notably releasing a fully-integrated protein structure prediction program in the earlier 2000s.

They began to expand into drug discovery, which led to the co-founding of Nimbus Therapeutics (later sold to Gilead) and collaborating with pharmaceutical companies such as Sanofi, Takeda, and notably, Agios, where SDGR’s software was used in Tibsovo and Idhifa, which are FDA approved cancer drugs.

They currently have six pre-clinical trials being conducted, three of which are in collaboration with Bristol-Myers Squibb

SLP’s drug discovery software is not physics-based. This leads to less accuracy when predicting molecular reactions, which then leads to less stable compounds, which then ultimately leads to a lower likelihood of commercialization. SLP also dedicates significantly fewer resources towards future innovation and improvements when comparing their research and development spending versus SDGR’s. This lack in R/D spending has allowed SDGR to gain market share while widening the economic moat surrounding their business.

SDGR has robust financials that are anchored by consistent growth, high margins, strong cash reserves, and a recent turn to overall cash flow positive. The consistency of their growth in the software business is highlighted by a steady 16% CAGR in ACV over the past 8 years. They have consistently been able to scale current customers to larger contracts along with bringing in new customers. Their strongest YoY growth in software revenue came in 2020 with a 38.65% jump;

A massive $202M cash position; this is largely due to the public offering from August of 2020, where the company sold 5.75M shares at a price of $66. Their cash position is further solidified with $440M in marketable securities, bringing their total current assets to $682M

They are cash flow negative from operations and investing

Pipeline Failures: If SDGR’s wholly-owned or joint drug discovery ventures are failures, this will cause a two-fold downward pressure on the stock- as investors will question the abilities of the software itself and will be pricing out the possible upside associated with the commercialization of a drug.

[Comments]

Using the software properly is a case of “clear only if known”. Setting all the parameters to account for all probable variables, in a way that achieves conformational agreement with experimental data appears to be one of SDGR’s chief problems (unless you’re an experienced computational chemist, I might add).

Theoretical chemists at large pharmaceutical companies are trained to take all the relevant parameters into account, as are academic computational chemists, but that’s not always the case at smaller institutions and drug discovery startups, nor is it generally true with older experimental chemists, even at the big Pharma companies. This is simply not what they’ve been trained to do or have been doing for 10 or 20 years.

My thesis then–there may be a kind of hard limit to software sales, based on the ability of end users to obtain actionable (accurate) data. If so, the key for me, as an investor, is– will primary SDGR investigations, collaborations and more service-oriented offerings (help in implementing and using software

They mention how they believe their software is not being used to the full extent by their customers, while SDGR is using it to the full extent in their own pipeline.

The experimentalists of tomorrow are all at University today training on Schrodinger and other computational programs. They’ll be far more proficient at it and won’t suffer from being part of a culture that cut its teeth in wet labs with lab coats and petri dishes.

In the end there will still be plenty of wet lab work to do, only it won’t waste billions of dollars and millions of man-hours on testing useless drug candidates. It will focus on those, which have been previously vetted and winnowed through computational programs.

1. A quick keyword search shows that there are a handful of public companies that consider themselves competitors to SDGR, but as you point out, none are competitive in the physics-based simulation that they have (which is a game changer in the space). Chemical-based “simulations” are a dime a dozen and solely reliant on the amount of data but do not compare to the real-world variant of the physics-based simulations.

2. SDGR has noted that it takes 1 GPU about 24 hours to run ONE physics-based simulation and now they run thousands or hundreds of thousands in parallel. Comparatively, in 2010, just one simulation took 3 weeks to run with their top rig. The technology itself did not really become viable until 2018, and it’s a story of accelerating feasibility. This will continue to shrink and within 3 years, they expect to run more simulations in a day than they are now able to do in a year.

Criticism of the $SDGR Platform

Experimental binding assays as means of testing drug candidates are nowhere near being replaced by computational predictions. And then, there is toxicology, immune response, pharmacokinetics, etc etc. There is indeed a promise of future computational progress, and SDGR is indeed one of the best bets for it. However, simply using buzzwords such as “physics” or “machine learning” doesn’t make it so. Many of the modern medicines are antibody-based, rather than small molecules, and the present SDGR tools are not even applicable to them. You don’t have to take my word for it but, as a business major, you would benefit from researching such things thoroughly, especially for something as specialized as pharmaceuticals. If you have any contacts involved in drug development research at any of the major pharmaceutical companies, you can ask them how they do their work and what they think about replacing experimental data with computational tools such as those from SDGR, not at some hypothetical point in the future, but at this specific moment. It’s a difference between the real world and investor presentations.

as of now, SDGR software they sell is not based on AI, it is old-school quantum physics. In terms of SDGR tools not being good enough for antibodies - yes, that’s true. Simulation software’s prediction fidelity is limited by the fidelity of the force field (there are other variables related to sampling efficiency but they can be overcome with faster hardware, so it’s doable). None of the physics based force fields available now are good enough at reproducing experimental data for large biomolecules. If you take an experimentally determined protein structure and subject it to a free molecular dynamics run, it will quickly start deviating, accuracy going down. Force fields based on quantum mechanics are better at this, but still not good enough and much more expensive, so you cannot afford to run long simulations with them. Even the best quantum mechanics tools we have now use significant approximations, so it’s not the way to go imo. Antibodies are large (150kDa) proteins with yet-uncharacterized intra- and inter-domain dynamics, so they are very hard targets for any simulation software. Improvements in AI as they train with more data - in principle that’s true. The problem is that we don’t have a single protein (or RNA ) where dynamics (rather than structure) has ben characterized experimentally, so there is nothing to train on right now.

DeepMind beat all of the best and brightest biomolecular simulations folks that were at it for decades, by entirely avoiding physics based force fields.

Use of SDGR’s platform by pharma/biotech companies does not mean they do not use other simulation software as well. Vast majority of bio-simulation people I know at places like MRK, GSK, NVS, or NVVX rely on CHARMm or Amber force fields for much of their work.

I think it’s because drug development is so drawn out, compartmentalized and heterogeneous. People involved in projects on different target would rarely interact and their challenges would be very different. In one case, a high quality structure of your protein target is available and you can run SDGR’s software of of it, and in another you may not even know what that protein structure is, so you’ll have to use another software that we did not even mention yet called Rosetta to predict the structure from scratch (from the primary sequence). When you are running such targets, your predictions are never going to be 100% reliable, so you’ll have to sample around them, and that’s where software like CHARMm or Amber comes very handy. Once you did this sampling, you can take the output models and use them as inputs into SDGR software. Yes, all of these processes will need to go through ligand optimization stage that SDGR does in silico (largely), with a promise of faster/cheaper solutions. As I mentioned before, one of their challenges is that they needs to move away from small molecule ligands as most pharma companies are now focusing on antibody-based pharmaceuticals. To give one example, everything I dealt with so far on binding to the covid-19 spike protein variants includes antibody domains. In its present state, SDGR would not be able to handle this. I am optimistic as they are so far ahead of the few rivals they have and I expect them to address antibody binding eventually.

Schrodinger: An Investment In Drug Discovery In Addition To Software Sales (Sep 2021)

[This write up (& the subsequent comments) is bit more of a technical overview]

Schrodinger has been able to port its already advanced software logic, on the best platforms to optimize computational power to extract valuable information from petabytes of data.

The company has more than 25 partnerships and is eligible for milestone payments from partners when candidates advance stages.

In this respect, drug discovery revenue was 5.7 million for the second quarter, compared to 2.2 million in the second quarter of 2020. This amount includes $3.3 million recognized from the collaboration with Bristol Myers Squibb (BMY) and a payment from a collaborator associated with the acquisition of intellectual property following the achievement of a lead optimization milestone.

As for CDC7 and WEE1, these two programs target cancer through replication stress and DNA repair mechanisms. First, some researchers think that CDC7 is related to cancer cells’ proliferative capacity and ability to bypass normal DNA damage responses. Consequently, targeting proteins that play roles in DNA’s replication strategy is gaining momentum as a therapeutic approach to combat cancer. Second, WEE1 is a tyrosine kinase regulator of the G2/M cell cycle checkpoint. When inhibited, it reduces cell viability by inducing apoptosis (death) of cancer cells. These programs are still at the preclinical phase and will take years to proceed to the commercialization stage.

Starting with the MALT1 inhibitor program, it is gaining increasing attention as a therapeutic strategy to treat certain relapse store resistant B-cell lymphomas and chronic lymphocytic leukemia.

operating expense was $42.3 million in Q2-2021 compared to $30.7 million in the second quarter of 2020. Also, the management is anticipating that full-year operating expense growth will be higher than the 42% annual growth rate seen in 2020.

I expressly mentioned Zai Lab as Schrodinger has exposure to PARP inhibitors through its partnership with the Chinese commercial-stage biotech. These have already demonstrated efficacy in multiple cancers, but new regimens and combinations that result in durable responses are needed, especially in patients who become resistant to treatment.

These PARP inhibitors are used in combinational treatment with chemotherapy and PD-1 antibodies by others in the clinic. Others are using PARP inhibitors combined separately with several agents, one of these being WEE1.

Interestingly, Schrodinger has identified multiple WEE1 inhibitors that are highly selective and show strong pharmacodynamic responses and anti-tumor activity in vivo (in the body). The company’s presence in DNA damage repair drugs therapy could be highly beneficial, with the market projected to grow at a CAGR of 18.4% during 2022-2027.

[Comments]

It’s not cheap to do your own drug discovery or constantly up your computational game through bigger and faster clusters.

I believe SDGR does have non-annual pricing options for its customers who run programs on its own system through tokens that entitle you to varying amounts of run time for various programs. Not sure about revenues generated by this business model.

Fact is that we won’t see any big revenue increases until SDGR begins hitting milestone targets on their major collaborations and, hopefully, in conjunction with that, starts selling higher numbers of licenses to existing customers.

They’re already selling to virtually all of big pharma. It’s just that the current contracts are mainly for theoretical chemists, while most pharma scientists are lab (experimental) chemists.

That will change over time (my thesis) as SDGR becomes THE go-to library screening product, effectively replacing most wet lab work snd as new hires with computational chem backgrounds and SDGR academic experience replace older lab scientists.

AI doesn’t do computational chemistry per se. Google doesn’t know computational chemistry and you can’t simply add an AI plugin for this kind of complex program, based on sets of mathematical transformations, where each job setup requires extensive knowledge of energy dynamics, structural considerations, etc. I don’t know of a single AI program that’s fungible and generic and simply “learns” from any kind of data and becomes expert at it. It’s application specific and requires detailed, expert knowledge within that field. It requires examples of what’s acceptable and what’s not. It requires rules and heuristics. It requires algorithms.

What AI, if properly developed, can definitely do, however, is take a computational chemistry product and make it more efficient through analysis and learning from the thousands of data sets for a particular target. It can certainly come to understand what’s working and not working so well and make recommendations based on that. It can also learn the process for setting up jobs and helping less sophisticated users in that regard. That’s a huge deal actually. See below.

One of SDGR’s biggest issues over the years is that top computational chemists routinely get computational results from SDGR software that conform very well to real-life experimental results. Not so, however, with your run-of-the-mill research facilities (think smaller colleges and Univ departments). Their results are all over the place.

The likely reason is lack of understanding of the many parameters that need to be set to run the jobs properly or poor execution. This is one reason (I believe) that SDGR finally decided to collaborate directly with Pharma companies by sending their own team of computational chemistry experts. They get far more accurate results this way and it’s a tiny expense for a BMY, when the result may be a unicorn drug.

AI-fueled wizards for SDGR products can help all chemists and biologists, especially less sophisticated ones, get better results by steering them towards best practices when setting up their jobs, drawing upon data sets contained in a large shared database.

If the product is friendly for experimental chemists (the ones who’ve been running hundreds of thousands of wet lab candidates through the mill) big pharma companies will buy all their chemists licenses, instead of just theoretical and the more savvy experimentalists.

This will dramatically boost software revenues. As more and more younger chemists get hired I expect this process to accelerate, because they’ll most likely already have some experience working with SDGR Glide (library screening for initial vetting/winnowing of massive numbers of drug candidates) and other software.

Several competitors are ahead on integrating AI to their platforms but still well behind on the science. Ideally SDGR crushes it by first getting some highly anticipated wins (FDA approval, positive Clinical trials, more big collaborations) and second, by scaling the product through AI to make it available to your average experimental chemist who’s more used to peering at petri dishes than setting parameters for FEP docking analysis jobs.

Battery tech sounds very exciting but quantum calcs of heavier elements are extremely challenging - there are no real good ways to deal with electron correlations.

Lithium batteries are not metallic lithium. The common compound at the cathode - lithium metal oxide is in fact LiCoO2, and Cobalt is plenty heavy for quantum calculations. At the anode, you have a graphene intercalation product, which in its simplest form can be represented as LiC6 (even though it’s actually a very poor approximation), and that’s 39 electrons in total. I have experience with quantum calculations on organometallic compounds and I can vouch for how difficult they are. The higher you go in the Periodic Table, the dicier it gets. Setting all that aside, if SDGR can make a productive contribution in battery research it would be a huge bonus.

Mathew D. Halls, Senior Vice President of Materials Science, is responsible for leading the materials science program at Schrödinger. Prior to joining Schrödinger in 2012, he was a senior scientist and account manager at Materials Design, Inc. and Accelrys, Inc. Before that he held the prestigious E.R. Davidson Fellowship in theoretical chemistry at Indiana University and earlier was the Manager of the Scientific Simulation and Modeling Group at Zyvex Corporation. Mat has worked with Fortune 500 companies to advance the adoption of atomic-scale materials modeling techniques in diverse industries including aerospace, electronics and specialty chemicals. He has made significant research contributions in areas such as computational spectroscopy, organic optoelectronic materials, nanocarbon-polymer interfaces, thin-film precursors and deposition processes and battery electrolyte additives; with his work being cited more than 5000 times.

Once computational methods are shown to work––once these collaborations bear fruit, that is, I fully expect that SDGR will become the leader in drug discovery software, which will quickly have a big fat TAM, as most scientists and every new Pharma hire will routinely have a license for these products.

So, think of the collaborations and the in-house drug discovery efforts as priming the pump for this massive transformation.

Again, the “both alive and dead” metaphor is appropriate, and, yeah, there’s an element of randomness, because the software could work perfectly to select a promising drug candidate, only to bomb out because it causes blood clots in certain demographic groups. Or an FDA scientist weighing in on the drug application (NDA) could have a really bad day, I suppose.

Until the box is opened to reveal a dead or alive kitty don’t expect any transformative technology. If the cat lives….THEN expect that every major pharma company will purchase licenses for all of its scientists (not just theoreticians), because margins will be just so much better (plus it’ll save precious time) using computational drug vetting rather than testing 100,000 compounds in a wet lab.

Competitors (Jan 2022 update)

https://seekingalpha.com/article/4478201-schrodinger-conviction-high-q4-report-guidance-critical

At the current market cap, SDGR’s internal pipeline is given zero value. The BMY partnership alone represents a potential of $2.7B in milestone payments, of which $1.7B is early-stage milestones, which is currently greater than the entire market cap of SDGR.

It takes a new customer about 12-24 months to build out an internal infrastructure and transition their legacy systems before they can truly ramp up licensing across their drug discovery programs.

[Comments]

Arguably the main competitor to SDGR is Evotec SE (a German company with Nasdaq-listed ADR of EVO). It is more than twice the size of SDGR in revenue (likely 2022 sales of $500 million) and is profitable. Price/Sales for 2022 may be around 11. My impression is that EVO is five years ahead of SDGR in terms of business model and execution (though not necessarily in terms of software technology). If I held SDGR stock I would be worried that the burden of expensive PhD employees scattered around the world would push (or maybe already has pushed) SDGR’s operating costs above a level at which profitability can be achievable in a competitive sales environment.

Evotec has the same “Science pool” idea.

They are really similar businesses, just Evotec has a more life sciences know how, mainly concerned with all the R&D a customer company can ask. They have a wide approach for all kinds of therapies, with a world leading IPSC system, good mAB manufacturing abilities in their JPOD etc etc. Their company presentation is really great.

They are also growing slower than SDGR. SDGR can hit a successful drug and explode in stock price while Evotec owns small royalties (from 130 drugs).

@biotech2k1 mentions $RLAY, $RXRX as part of AI Drug Development Landscape:

“$RLAY licensed the $SDGR software then went out and bought and built more software for drug development. They have a pipeline that is taking on some of the hardest targets in oncology like PI3Ka and FGFR.”

“$RXRX uses robots doing experiments to record millions of experiments. They are an automated lab. All that data is collected into a supercomputer that uses software to guide drug development. They have 4 drugs moving into phase 2 with many others in early development.”

What are the risks? SDGR may be modeling irrelevant aspects of molecular structure, for example. With improved computer speed less sophisticated but similarly valid software may be developed by other companies or in-house by big pharma, for example.

Modeling yesterday’s targets can be irrelevant, e.g., fading relevance of mAbs. Much of SDGR’s 20 years of modeling may be largely irrelevant.

In Search of Value in AI/ML Based Drug Development (Dec 2021)

Valuation of $SDGR as on Jan 2022 - @Biotech2k1

“Taking a look at the value in $SDGR. This company has 2 parts. The first is the software business which licenses the software used in CAD of proteins and enzymes.

The projected revenues for 2022 is $194 million. That makes this company only 10x revenues which is actually cheap for a software company. Their entire market cap is only $1.9 billion. They have $600 million in cash.

They also have a pipeline of 3 wholly owned drugs that should be going into phase 1 trails. They also have multiple partnerships with big pharma like BMY, Takeda and Zia Labs. If you buy them here, you are getting a cheap software company and the biotech pipeline for free.”